The Real Real Merchandise Scandal: Inventory and Consignment Sales (Blog Post with Graphics)

Is that luxury item you purchased the genuine article?

If not, you’ve overpaid by a wide margin.

That’s was the scandal at The Real Real, world’s largest online consumer marketplace for luxury items. The company website states that the firm “is the leader in authenticated luxury consignment. Every items we sell is 100% authenticated by an expert.”

The company’s value proposition is that, when we sell you something, it’s the real thing.

Unfortunately, that’s not always the case. The resulting scandal is a great tool to explain accounting for inventory.

Contents

What happened

A 2019 CNBC investigation found that: “many of the items on the site were being authenticated by copywriters with limited training, leading to mistakes.” In fact, the company produced an internal report, called “Copywriting Faux and Tell,” that served as a “weekly recap of TRR published and returned counterfeits.”

Ouch.

The firm’s stock price declined by over 35%.

The Real Real operates on a consignment basis. What does that mean?

Consignment accounting

Accounting Tools defines consignment:

“A consignment occurs when the owner of goods leaves them with another party to be sold. When the goods are eventually sold, the consignee retains a commission and pays the consignor the residual amount. Consignment arrangements are relatively common for certain types of retail sales. Online auction sites are a form of consignment arrangement, since a third party is undertaking the sales role.

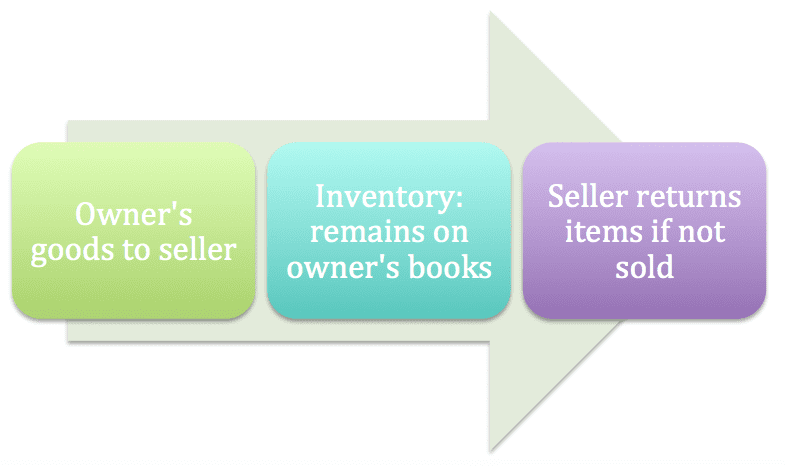

In a consignment arrangement, the consignor continues to own the goods until they are sold, so the goods appear as inventory in the accounting records of the consignor, not the consignee.”

An example

Let’s assume that Upscale Clothing has 500 Kate Spade purses that are consigned to The Real Real (TRR). The two parties agree that the purses will be priced at $100 each, and Upscale sends the purses to TRR.

In accounting terms, Upscale is the consignor (the party providing the goods), and TRR is the consignee.

Assume that Upscale Clothing’s cost per purse is $70, and that TRR agrees to sell the purses for $100 in cash. Upscale will pay TRR a $10 commission for each purse sold.

Upscale still owns the inventory, and no sale has taken place. However, TRR now has possession of goods owned by someone else. If the goods are not sold, they must be returned.

TRR needs to post a liability for the consigned goods received:

Debit consigned inventory-purses $50,000 ($100 X 500 purses)

Credit accounts payable $50,000

Note: Consigned inventory is not an asset account on TRR’s books, it’s a “holding place” to account for goods held for another party.

Recording a sale

Here are the entries when the 100 purses are sold for cash:

Upscale’s books

The inventory balance is reclassified to cost of sales:

Debit cost of sales $35,000 ($70 cost X 500 purses)

Credit inventory-purses $35,000

A sale is recorded, along with a commission expense.

Debit accounts receivable $45,000

Debit commission expense $5,000 ($10 commission X 500 purses)

Credit sales $50,000 ($100 sale price X 500 purses)

The profit to Upscale is:

$50,000 sale – $35,000 cost of sales – $5,000 commission = $10,000

TRR’s books

#1 TRR receives cash and records a sale

Debit cash $50,000

Credit sales $50,000

#2- TRR moves reclassifies the consigned goods balance to cost of sales:

Debit cost of goods sold $50,000

Credit consigned inventory-purses $50,000

#3- TRR pays Upscale, less the commission amount earned, and removes the liability balance:

Debit accounts payable $50,000

Credit commission income $5,000

Credit cash $45,000

The profit to TRR is:

$50,000 sale + $5,000 commission – $50,000 cost of sales = $5,000

TRR’s profit is only the commission received on the consigned goods.

For more content on accounting, finance, and entrepreneurship, join Conference Room for free.

Go to Accounting Accidentally for 540+ blog posts and 450+ You Tube videos on accounting and finance:

Good luck!

Ken Boyd

Author: Cost Accounting for Dummies, Accounting All-In-One for Dummies, The CPA Exam for Dummies and 1,001 Accounting Questions for Dummies

(email) ken@stltest.net

(website and blog) https://www.accountingaccidentally.com/