How to Use Activity-Based Costing (5 Video Links)

Not all costs can be assigned directly to a product or service, and that makes it harder to compute the total cost for an item that you sell.

Say, for example, that you manufacture baseball gloves. You spend money to purchase leather as a raw material, and you incur labor costs to run machinery and to package baseball gloves. Calculating these direct costs is straightforward.

But what about the utility costs for the factory? These indirect, or overhead costs, are more difficult to assign to a baseball glove. That’s why companies use activity-based costing.

Contents

Activity-Based Costing Definition

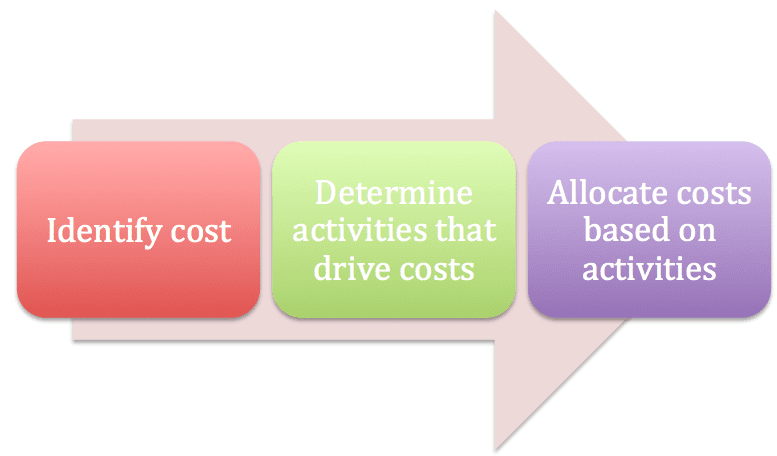

In my Accounting All-In-One For Dummies book, I explain that activity-based costing (ABC) allocates indirect (overhead) costs based on an activity level. ABC helps a business to assign costs more specifically, so you can compute the total cost of a product, and price the item to generate a profit.

Sure, you may assume the evenly spread costs over a group of customers, or based on a number of sales. But if some sales require more effort than others, those sales should be assigned more costs.

Activity-Based Costing Example

To explain the benefits of ABC costing, assume that Julie owns Fine Food Distributors, a company that supplies meat, fish, and poultry to restaurants. Julie needs to allocate $50,000 in salary and benefits paid to the company’s order manager.

Activity-based costing formula

One option is to evenly distribute the cost over the total number of orders received during the year. ($50,000 / 2,000 orders) = $25. The number of orders is referred to as the cost object. Every order is allocated $25 of overhead for the order manager. This strategy is referred to as peanut butter costing- you spread costs evenly, like spreading peanut butter on bread.

But what if some customers require more time and effort than others?

Join Conference Room for free. Great content on accounting, finance, and humor/ short story topics.

Why you should use ABC costing

Overhead costs should be assigned based on the activities required to deliver the product or service to a particular customer.

Fine Foods has 15 clients that generate 90% of the revenue, and two clients require more time and effort. These clients change orders at the last minute, which requires Fine Foods to cancel the original invoice an generate a new one. The staff also must remove items from the delivery truck, put some items back in inventory, and add new items. All this work must be changed in the accounting and billing system.

Fine Foods decides to track the time incurred per customer, and charges an additional fee for the time and effort required for a changed order. The $50,000 order manager cost is allocated based on time spent per order, not spread over all orders. As a result, the problem clients are assigned more costs.

The benefits of using ABC costing

When you use ABC costing, you overhead costs are assigned more precisely, and you have a more accurate measure of total costs. You can use the new total cost number to price your product, and your profit calculation is more accurate.

Here’s another example of ABC Costing:

Reviewing the Morgan Stanley Purchase

Buying another firm may create synergy, which can lead to higher sales and profits. The combined firms can produce better results than if each business operated separately. But if you don’t get costs assigned correctly, you won’t know if a company purchase is working as planned.

Morgan Stanley’s 2020 purchase may be wise move.

What Happened

As the Wall Street Journal wrote:

“Morgan Stanley is buying E*Trade Financial Corp in a $13 billion deal that will reshape the storied investment bank and firmly stake its future on managing money for regular people.

E*Trade brings five million retail customers, their $360 billion in assets and an online bank with cheap deposits that Morgan Stanley can funnel into loans.

Its crown jewel is a comparatively low-profile business: managing the stock that employees at hundreds of companies receive as part of their pay. Those shares are typically locked up for a few years and when they become available, E*Trade aims to move those employees into brokerage accounts.

Morgan Stanley expects to recoup that premium through $400 million of cost cuts and additional savings of $150 million from using E*Trade’s low-cost deposits to replace more expensive funding.”

Why The Purchase Made Sense

Morgan Stanley can generate interest income on loans from E*Trade’s online bank deposits. The firm also has a potential pipeline of new brokerage business from stock awarded to employees as deferred compensation.

But the key to making the purchase work is cutting costs. You can’t intelligently reduce costs unless you understand the source of the spending.

Think about it.

The two firms will eliminate duplicate costs. There’s not longer a need for two accounting departments, two legal staffs, two payroll firms. Sure, there’s more work to be done in a much larger company, but some roles will overlap and not be necessary.

Go to Accounting Accidentally for 600+ blog posts and 450+ You Tube videos on accounting and finance:

Before the combined firms start cutting costs, management needs to take a careful look at the activities that cause expenses to be incurred.

Deciding on Activity-Based Costing

Once again, activity-based costing (ABC) allocates costs based on an activity level. ABC helps a business to assign costs more specifically.

Consider the stock-trading department for the combined firms.

Morgan Stanley and E*Trade serve different types of investors, but each company needs traders who can buy and sell stocks for clients. Now, much of the activity is automated, but the sheer volume of trading requires an investment in technology, and smart people who can monitor trading, and get the right trades assigned to the correct investors.

So, how can you allocate the stock-trading department costs?

By thinking about the activities that require more time and effort.

Morgan Stanley caters to larger clients, including institutions, who are placing much larger trades than individual investors at E*Trade. Larger trades involve more risk, and more effort to get the customer the right price.

If the stock-trading department spends 60% of its time on Morgan Stanley trades, 60% of the cost may be allocated to Morgan Stanley.

Other examples of ABC costing:

- Legal costs are allocated, based on the total time spent on legal cases between the Morgan Stanley and E*Trade.

- Payroll costs are assigned based on the number of employees at each company division.

Before you start to cut costs after a merger, you need to understand the activities that cause the businesses to incur expenses. If not, you may cut cost in the areas that drive the most revenue.

Food for thought.

Good luck!

Ken Boyd

Author: Cost Accounting for Dummies, Accounting All-In-One for Dummies, The CPA Exam for Dummies and 1,001 Accounting Questions for Dummies

(email) ken@stltest.net

(website and blog) https://www.accountingaccidentally.com/

Image: Dmitry Moraine