The Lemonade Stand and the Mutual Fund Expense Ratio

“Lemonade Stand 100 feet.”

If you’re selling lemonade, put your stand 100 feet from a playground- smart marketing.

Doing business comes with costs, obviously, and expenses that you must incur each year can sharply reduce your profit. The same is true of mutual fund fees and expenses that lower an investor’s rate of return.

I’ve written about market risk, stock price volatility, and the risks of do-it-yourself investing. However, don’t forget about the fees you pay to invest- they make a huge difference in your earnings.

Contents

Types of mutual fund costs

There are several types of costs you may pay for owning a mutual fund:

- Sales charge: A cost you pay when you purchase the fund. The sales charges (or sales load) may be assessed when you buy the fund, or when you withdraw funds after purchase.

- Annual expense: Most mutual funds charge an annual expense to cover the day-to-day cost of managing the fund (accounting, legal, money management). This fee is based on a percentage of assets under management.

- 12B-1 fee: Investopedia defines this cost as an annual marketing or distribution fee on a fund. This fee is also based on a percentage of assets under management. A 12B-1 fee can be used to compensate the salesperson for monitoring the fund’s performance and answering client questions.

When it comes to costs, investors should use the mutual fund expense ratio to assess the true cost of a mutual fund over time.

More great content on accounting, personal finance, and humor/short stories. Join Conference Room.

Mutual fund expense ratio definition

Bankrate defines the expense ratio as “the cost of owning a mutual fund or exchange-traded fund (ETF). Think of the expense ratio as the management fee paid to the fund company for the benefit of owning the fund. The expense ratio is measured as a percent of your investment in the fund.”

Here’s a mutual fund expense ratio example: If the fund charges 0.45 percent, you will pay $45 for every $10,000 invested in the fund. Important: this fee is charged annually, which is why the expense is so important. If you own the fund for 30 years to save for retirement, you’ll paying the fee every year.

Mutual fund expense ratio explained

How do your find a fund’s expense ratio?

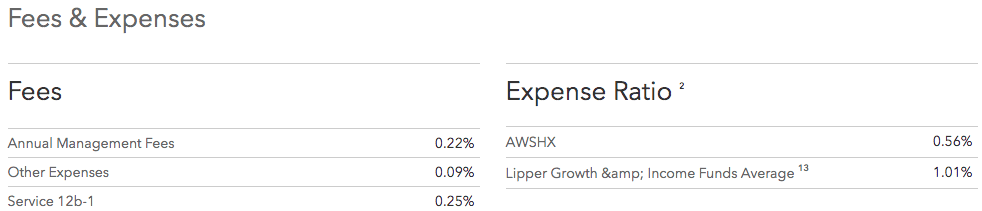

The disclosure of mutual fund costs has improved over the years, and the easiest place to review your fund’s costs is the website. Here’s a link to the American Fund’s Washington Mutual page. If you click on “Fees and Expenses” you’ll find the expense ratio (as of 8/25/22):

The mutual fund expense ratio formula is the sum of management fees, other expenses, and the 12B-1 fee, totaling 0.56% (top right). The fund also provides a mutual fund expense ratio comparison, showing that this fund’s expense ratio is less than the average of similar funds (which charge 1.01%).

That’s a big deal.

This mutual fund is charging 0.45% less than comparable funds- those with similar investment goals. Over time, as you accumulate a bigger balance, the dollar amount you save on expenses can be thousands of dollars- or more. The savings increase your total assets over time.

Pressure to pay more fees

In 2015, the Wall Street Journal pointed out the SEC’s concerned about mutual fund fees that may not be fully disclosed. A large percentage of mutual funds are sold through financial advisors. Those advisors, obviously, want to maximize the compensation they get for selling and managing money in a mutual fund.

The SEC was concerned that mutual funds may be making extra payments to pay advisors for additional services. One such service is the process of consolidating the trading records for an advisor’s clients. If recordkeeping can be improved, that feature benefits the financial advisor. However, those services should be paid for by the advisor’s firm- not the mutual fund company.

Extra payments, possible conflicts

Regulators are concerned about a fund paying an advisor for these extra services. Those payments may influence the advisor to sell the fund- even though another fund (that doesn’t pay for those costs) is more suitable. FINRA limits the spending on marketing and distribution, based on the average net assets of the fund.

Why costs matter

Two costs have a huge impact on your mutual fund’s rate of return: Taxes and fees. While your fund does not need to have the lowest fees in the industry, their costs should be reasonable- when compared with similar funds.

Check your costs, monitor your fund’s return

Make the effort to read your fund’s summary prospectus. Mutual fund websites now present easy-to-read information. Morningstar is also a great tool to assess your mutual fund. This service ranks mutual funds against their competition.

Take these steps to manage your investment. While you don’t need to read everything, you can stay informed and make smart investment decisions. As always, consult with a financial advisor regarding personal finance decisions.

Ken Boyd

St. Louis Test Preparation

Author: Cost Accounting for Dummies, Accounting All-In-One for Dummies, The CPA Exam for Dummies and 1,001 Accounting Questions for Dummies

(email) ken@stltest.net

(website) https://www.accountingaccidentally.com/

(you tube channel) kenboydstl